How Agility Enables Innovation

GUEST POST from Diana Porumboiu

In the previous article on agile innovation we covered the main concepts around agile, business agility and its role as a driver for innovation. Now, let’s see how to actually leverage agility to innovate and how other companies have succeeded in this area.

Agility is an enabler for innovation. The pace of innovation, while not easy to achieve, has become the ultimate competitive advantage as we all need to adapt quickly to evolving environments, the digital age and increasing pressing needs.

The reality is that agile thinking is changing the world whether we decide to adopt it or not.

Those who succeed at this are ahead of the game. McKinsey research suggests that agility is a critical factor for organizational success.

The Organizational Health Index (OHI) assesses various aspects of organizational health, including agility, and examines how these factors correlate with business success. An increased organizational health is linked with more resilient, adaptive, and high-performing organizations that can better navigate complexity, drive innovation, and achieve strategic goals.

What’s more, agile organizations are best at balancing both speed and stability, and these are also the companies that rank highest in the organizational health index.

The research goes even deeper and identifies a series of management practices that differentiate the most from the least agile companies.

As you can see, there’s more to business agility than meets the eye and a few sprints just won’t cut it.

However, if we look at the agile principles, there are several ways in which they can enable innovation:

- They bring an empirical process control approach, which emphasizes transparency, evaluation, and adaptation.

- They enable experimentation and learning as teams are encouraged to test hypotheses, validate assumptions, and learn from both successes and failures. This experimental mindset is essential for innovation.

- They are about adaptive planning processes that allow teams to adjust their priorities, strategies, and product roadmaps based on emerging opportunities and threats.

- They emphasize customer-centricity. By focusing on delivering value to customers through continuous delivery and customer feedback loops, you make sure your innovations meet real market demands and solve genuine problems.

- They encourage cross-functional collaboration and self-organizing teams, bringing together diverse perspectives and expertise.

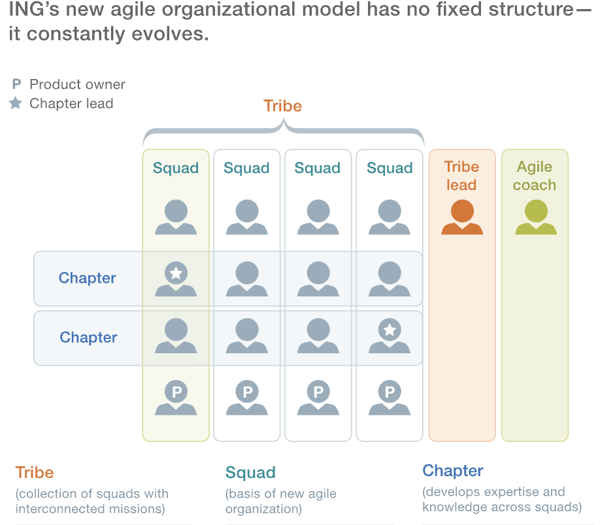

To get a better idea of how this looks in practice, we’ll take the example of ING Bank.

ING Bank

ING is a global financial institution originally from the Netherlands and a good example to illustrate how agile can be introduced organization-wide, the right way.

ING wanted to become agile for the right reasons. The shift to agility wasn’t about working faster or growing more—it was about being flexible and adaptable. Even though things were going well financially in 2015, ING noticed that customer behavior was changing due to trends in other industries, not just in banking. So, they knew they had to change too.

ING Bank embraced several key principles of agility, drawing inspiration from the practices of tech companies to align with their objectives and operations:

- Cross-Functional Teams: ING structured its IT and commercial departments into agile squads, mirroring the approach seen at Tesla. This integration fosters cross-functionality and collaboration, with teams physically situated together within the same premises.

- Rapid Decision-Making and Experimentation: Without bottlenecks created by middle management, ING facilitates swift decision-making and continuous experimentation. This agile approach enables the organization to constantly refine and test customer offerings without bureaucratic delays.

- Enhanced Collaboration and Transparency: Recognizing the importance of collaboration, ING implemented structural changes to break down silos. Clear delineation of roles, responsibilities, and governance structures fosters improved cooperation across teams and departments.

- Accelerated Delivery: Instead of their usual annual product launches, ING adopted a more agile release cycle, rolling out software updates every two weeks. This agile delivery model allows the organization to respond promptly to market demands and customer feedback, ensuring rapid innovation and adaptation.

The first step in achieving this agile transformation was to develop a clear strategy and vision. They started small and rolled out the new structures and way of working across the entire headquarters in eight to nine months.

Last, but not least, they invested significant energy and leadership time in fostering a culture of ownership, empowerment, and customer-centricity, which are foundational elements of an agile culture.

As Bart Schlatmann from ING points out, agility is a means to an end, not the end goal itself; it is the pathway to achieving innovation.

Drawing from these examples and research from other organizations, we can summarize the five tenets of agile organizations:

- Purpose-Driven Mindset: Shift from a focus on capturing value to co-creating value with stakeholders, embodying a shared vision across the organization.

- Empowered Network of Teams: Transition from top-down direction to self-organizing teams with clear responsibility and authority, fostering engagement, innovative thinking, and collaboration.

- Rapid Learning Cycles: Embrace uncertainty and continuous improvement through iterative decision-making and experimentation, prioritizing quick adaptation over rigid planning.

- Innovation Culture: Cultivate ownership, empowerment, and customer-centricity, enabling employees to drive organizational success.

- Integrated Technology Enablement: View technology as integral to unlocking value and enabling responsiveness to business and stakeholder needs, leveraging advanced tools for seamless integration and rapid innovation.

Actionable Steps to Drive Innovation through Business Agility

We can’t wrap things up without going through some of the key steps that should not be missed in an agile transformation journey.

Constancy of purpose

You might have heard of Edwards Deming and even used his PDCA cycle in your continuous improvement work. He is well known for his legacy in the field of quality management, particularly for his contributions to the improvement of production processes in Japan after World War II. To some degree, his work is also seen as one of the main inspirations for the agile movement.

Among his work, we can also find the “14 Points for Management,” where Deming outlines how essential it is to have a clear and unwavering commitment to a long-term vision or mission.

He called it constancy of purpose. You can also call it your North Star. Regardless of the words you choose, it’s important to set your goals and align all activities, processes, and resources towards achieving them. How to do this?

- Communicate the Purpose: Regularly communicate the organization’s purpose, mission and goals as well as how agility contributes to achieving them.

- Define Goals: Clearly define objectives and goals that align with the organization’s purpose. These goals should support the overall mission and vision.

- Empower Teams: Trust by default and enable teams to make decisions, take ownership of their ideas and work. Provide them with the autonomy and resources they need to innovate and deliver value.

- Measure Progress: Measure progress towards your goals, but also establish metrics that can measure your ability to be responsive. Regularly review and assess how agile practices are contributing to the overall mission.

- Adapt and Iterate: Embrace continuous improvement processes that align with your internal structures and needs. Encourage teams to experiment, learn, and iterate on their approaches.

Agile leadership

Adopt the ABC of leadership which drives innovation and makes the shift from “vertical ideology of control” to “horizontal ideology of enablement”.

Linda Hill, renowned professor at Harvard Business School, specializing in leadership and innovation makes a great point about the roles a leader should take if they want to drive innovation and agility.

Over time leadership evolved from a purely strategic role, to providing a vision that guides people in the same direction. More recently, research showed that a visionary leader is not enough. You need leaders that can also shape the culture and capabilities needed for people to co-create the future. This requires a different approach to leadership.

Research has identified that in order to lead an organization that innovates at scale with speed, you need leaders that fill in three different functions:

- the Architect – to build the culture and capabilities necessary to collaborate, experiment and work.

- the Bridger – to create the bridge between the outside and the inside of the organization by bringing together skills and tools to innovate at speed.

- the Catalyst – to accelerate co-creation through the entire ecosystem.

Here is Hill’s short summary on the ABC of leadership:

Another top voice is Steve Denning who has been an advocate of agile and agile management for years. He makes some great points about the agile mindset which requires a new way of running organizations.

For an organization to be truly agile, the so called industrial-era management needs to be replaced with digital-age management which is strongly driven by an agile mindset.

The traditional management style makes it hard for agile to work because the old command-and-control approach goes against the agile principles. The top-down approach is riddled with bureaucracy which obstructs visibility to the customer and the realities at the lower levels of the organization.

Some of the most successful and innovative organizations, like Apple, Google, and Microsoft understood this early on and shifted their focus to delivering customer value first, one of the agile principles. This required a change in mindset but also in the corporate culture, which is no easy undertaking.

To make this transition, Denning talks about five major shifts that companies need to make:

- From profit-focused to customer-focused goals.

- From direct reporting to self-organizing teams where management’s role is not to check on employees, but to enable them to do their work by removing obstacles.

- From bureaucracy, rules, and reports to work coordinated by Agile methods and customer feedback.

- Prioritize transparency and continuous improvement over predictability.

- Encourage horizontal communication rather than top-down directives.

While they are straightforward and make sense for most of us, these changes are maybe the hardest to make, especially for established organizations that are not used to challenging the status quo.

These big undertakings are what make agile possible at scale. But even if you’re not there yet, you can still apply the agile principles at a smaller scale to enable innovation.

Minimize complexity

Complexity is the enemy of agility. People in companies both large and small try to come up with the perfect solution, that often doesn’t exist in the first place, and only end up having solved the wrong problem.

On the other hand, if you were to simply move ahead quickly with something that creates real value and solves at least some of the problems, you’ll see which of your assumptions and concerns are real, and which aren’t. You’ll also see which problems you can work around, and which ones you simply must address directly.

This obviously eliminates a lot of uncertainty and reduces the complexity associated with solving the problem, which again helps you focus your innovation efforts on what matters – creating real value.

The bigger and more complex the problem, the more important it is to take an agile and modular approach.

Thus, the bigger and more complex the problem, the more important it is to take this agile and modular approach that focuses on the speed of making tangible progress.

Conclusion

As we explained in our complete guide to innovation management, there is no single perfect way of managing innovation. Different companies have different approaches for innovation management.

However, the common thread of successful organizations are structures and processes that mitigate the somehow chaotic nature of innovation management.

In these two articles we explored agile as a method to enable innovation and improve its management for sustained success. We don’t believe in quick fixes or miracle solutions. That’s why we made the case of agile as a mindset that should permeate every aspect of the organization.

Article originally published in full format on viima.com/blog

Image credit: Unsplash, McKinsey

![]() Sign up here to join 17,000+ leaders getting Human-Centered Change & Innovation Weekly delivered to their inbox every week.

Sign up here to join 17,000+ leaders getting Human-Centered Change & Innovation Weekly delivered to their inbox every week.

Drum roll please…

Drum roll please…