by Braden Kelley and Art Inteligencia

This is usually the last question someone asks before they’re ready to move forward, which means it deserves a direct answer rather than the consultant’s reflex of “it depends.” It does depend — but on a small, specific set of factors, and I’d rather walk you through exactly what they are than make you guess.

The honest answer: it scales with scope, not with company size

The biggest misconception I run into is that audit cost tracks with company revenue or headcount. It doesn’t, directly. It tracks with the shape of the journey being audited: how many distinct touchpoints are in scope, how many channels the experience spans (in-person, phone, web, app, in some combination), and how many stakeholder groups need to be interviewed to understand the journey from more than one angle. A single-channel, single-audience journey for a mid-size company can cost less than a sprawling omnichannel journey for a smaller one, if the omnichannel journey is genuinely more complex to walk.

The five activities that drive cost

- Audience research and persona validation. Every audit starts by identifying your distinct audience segments and validating their journeys against current reality — surfacing the needs, expectations, and pain points that internal assumptions have obscured. One clearly-defined audience is a much faster starting point than four segments that each need their own research and validation pass, and this is usually the first scope decision worth making deliberately.

- Journey mapping and touchpoint analysis. From there, we create or update persona-based journey maps — identifying key touchpoints, pain points, emotional highs and lows, and improvement opportunities across every relevant channel. A journey with four or five touchpoints in a single channel maps far faster than one spanning fifteen touchpoints across phone, web, app, and in-person combined.

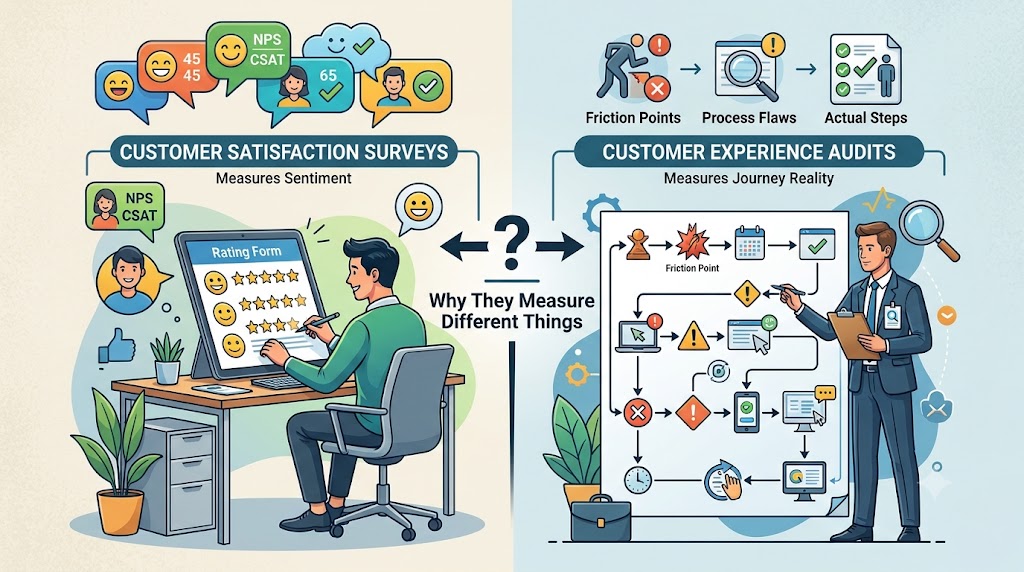

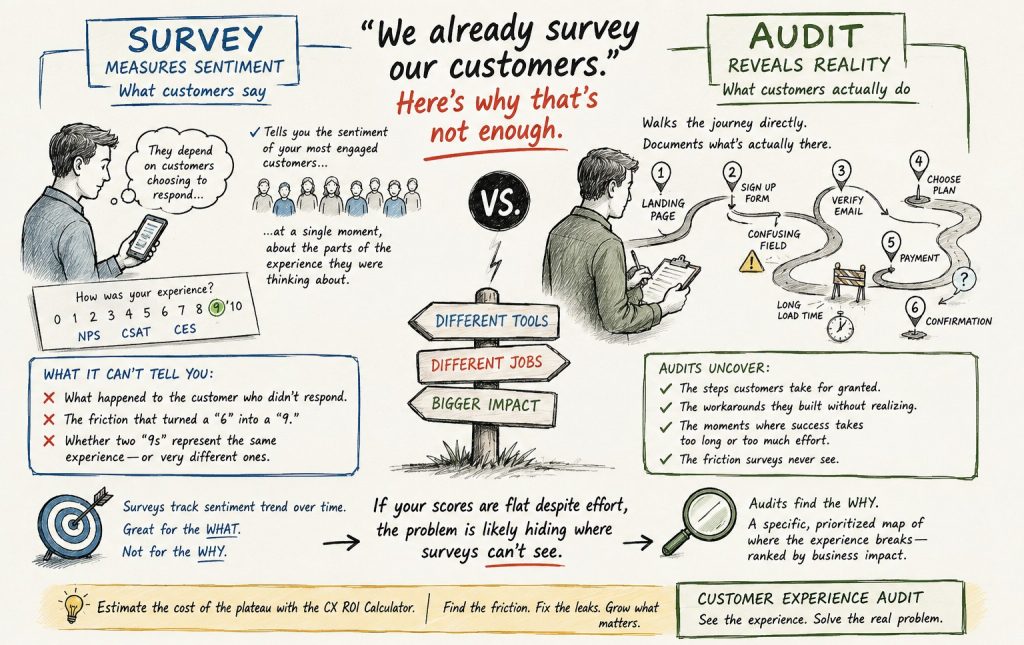

- Existing data evaluation. Your current KPIs, NPS scores, CSAT data, and sentiment analysis get analyzed for the patterns, gaps, and untapped insights that current reporting isn’t surfacing. How much historical data you already have — and how much of it is usable versus scattered across disconnected systems — changes how much work this step takes before it produces anything actionable.

- Walking the journey. This is where key touchpoints get evaluated firsthand — retail locations, digital channels, service calls, sales cycles, in B2B and B2C contexts alike — and it’s typically where an audit finds its most surprising and valuable insights. It’s also usually the most time-intensive of the five activities, because it’s genuine fieldwork rather than analysis of what already exists, and cost scales directly with how many touchpoints and channels get walked in person versus reviewed through documentation alone.

- Competitive benchmarking. Benchmarking your experience performance against select competitors and best-in-class examples shows not just where you stand, but how far you are from where you need to be. This one is genuinely optional depending on your goals — skipping it keeps the engagement focused purely on your own gaps, while including it adds real value when you specifically need to know how you compare to the alternatives your customers are weighing.

Timeline compresses or expands the cost of all five at once: doing them in two weeks instead of six doesn’t reduce the work, it concentrates it, usually by putting more people on it in parallel. If you have flexibility on timeline, it’s often the easiest lever to pull to manage overall cost.

The number that actually matters more than the price

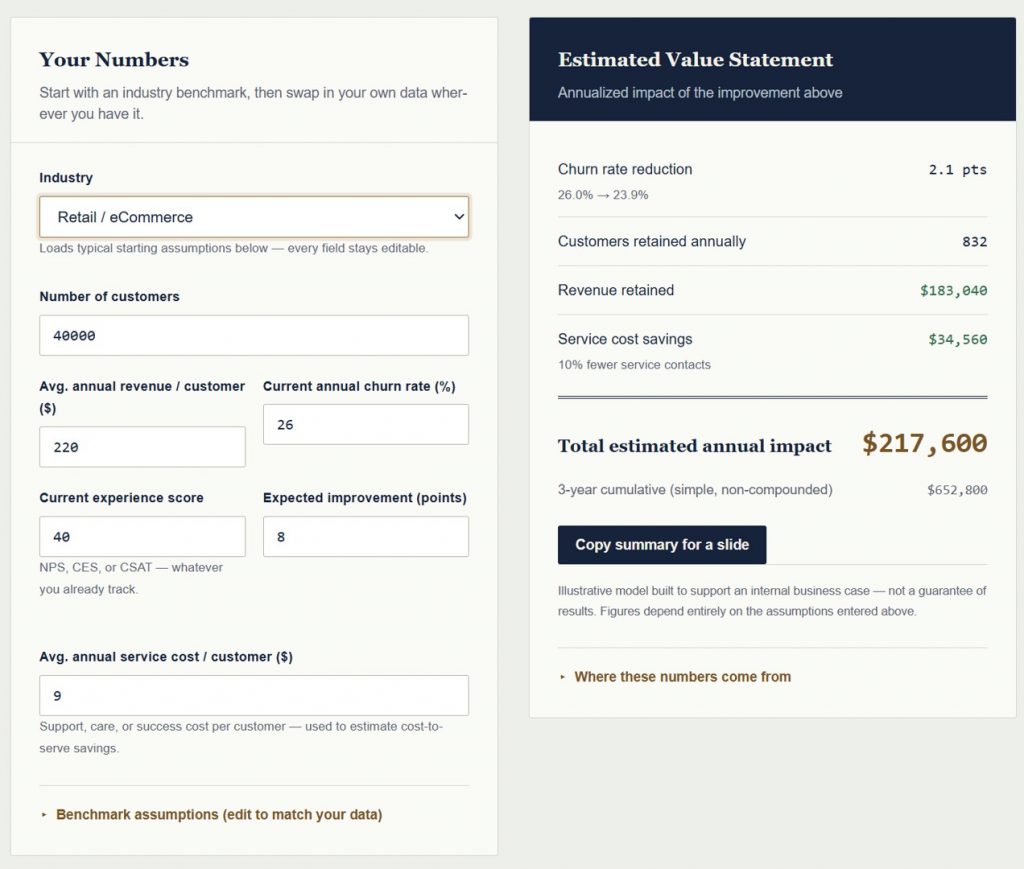

Cost in isolation is the wrong comparison. The comparison that matters is cost against what the friction is currently costing you in retained revenue, referral loss, and cost to serve — because that’s the number an audit is designed to protect. If you haven’t run that comparison yet, the CX ROI Calculator will give you a real figure in a few minutes, and it’s the right first step before a cost conversation, not after it. A number that’s larger than the audit’s cost is the fastest way to know the conversation is worth having at all.

Getting an actual number

Because cost depends on the scope decisions above, and those decisions are specific to your journey and your goals, the accurate way to get a real figure is a short scoping conversation rather than a published price list that would be wrong for most people who read it. If you’re at the point of wanting that conversation, the audit page has the details on how an engagement runs, and I’m glad to talk through scope and a realistic estimate directly.

Image Credits: Gemini

Content Authenticity Statement: The topic area, key elements to focus on, etc. were decisions made by Braden Kelley, with a little help from Claude to clean up the article.

![]() Sign up here to get Human-Centered Change & Innovation Weekly delivered to your inbox every week.

Sign up here to get Human-Centered Change & Innovation Weekly delivered to your inbox every week.

Drum roll please…

Drum roll please…