GUEST POST from Geoffrey A. Moore

For high-tech in much of the 20 century, when start-up capital was scarce and the need for it was great, innovation began at the core and migrated to the edge. Today we have the reverse. Start-up capital is plentiful, the need for it is modest, and innovation is thriving at the edge and moving reluctantly to the core, fearful of the inertia it will encounter once it gets there.

Yet if innovations are going to scale, they must leverage the core-edge dynamic in both directions. That means, in addition to enabling innovation from the bottom up—something today’s start-up enterprises are having great success in doing—we must also be able to manage it from the top down, from the core out, from the acquiring-sponsoring enterprise to acquired-innovating start-up. Here success is not so widespread, but there is a fix for that.

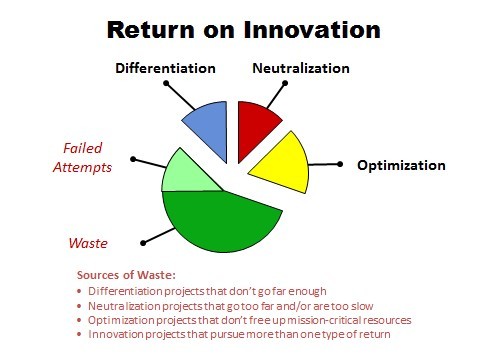

In the core-edge dynamic, the job of the core acquiring institution is not to innovate—it is to get a return on innovation from wherever it is sourced. This could be an internal skunk works project, a major R&D project, a tuck-in acquisition, or a merger with another mature enterprise. The challenge is not, in other words, to bring innovation into existence but rather to capitalize on it in a meaningful way. That is what the pie chart above is all about.

The key claims of this model are 1) that there are three ways to get a positive return from an innovation investment and 2) that they are mutually exclusive. (There are also at least five ways to get a negative return which we will get to in a moment.)

The winning returns can come from:

- Differentiation. To win here you must create an offer that dramatically outperforms its competitive set on at least one vector of innovation. You are playing for competitive separation, looking for a 10X result on at least one chosen vector, either in product performance, customer delight, or operational savings. This sort of thing creates the highest return on innovation possible. Think Apple iPad over any prior tablet (or arguably any tablet since).

- Neutralization. To win here you must catch up to a competitor’s innovation sufficiently to get your offer back in the hunt. This means getting to “good enough” as quickly as possible. Here you are playing for speed—how fast can you get back in the game. Think Google Android catching up to (and then overtaking) the Apple iPhone.

- Optimization. To win here you produce essentially the same offer on a better, faster, cheaper basis. Basically, you are extracting resources from an established effort in order to hit a new price-point, repurpose them for innovation elsewhere or simply taking to the bottom line. Here you are playing neither for separation nor for speed but rather for money. Think Nokia’s long history of success with feature phones.

The critical thing to note about these three sources of return is that they are at odds with one another. If you are going to get maximum separation, you cannot tell exactly when that will occur, so you cannot play for speed. Conversely, if you are playing for speed, you must suppress any impulse to go beyond a “good enough” standard. But in both cases you are willing to spend extra money to achieve your primary goal, be that separation or speed. That puts both approaches at odds with optimization, where the goal is to extract cost from the system.

The net of this is that top-down management of innovation requires leaders to charter their innovation teams with one—and only one—of these objectives. Where you have multiple needs, you need multiple teams. To understand why, let’s turn to look at how innovation investments fail to pay off.

There are at least five ways this can happen, as follows:

- The innovation doesn’t work. Ouch. But that is the price of playing innovation poker. In fact, if you have no failed experiments, you probably are not taking enough risk.

- The differentiation doesn’t go far enough. Yes, you create something different, but it is a far cry from a 10X separation, and so the market accepts it as good but does not grant you any competitive advantage for it. Basically, you just spent your R&D budget and have nothing to pay you back for it. HP and Dell have both suffered here greatly in recent years.

- The neutralization doesn’t go fast enough. The team got caught up in out-doing the competition rather than simply getting to good enough. The problem is, the market will not pay you any return on improvements beyond good enough, so all you have done here is waste time, which is the one thing you cannot afford to waste when your product is out of the game. Nokia was a prime offender here with respect to its tardy response to the iPhone challenge.

- The optimization doesn’t go deep enough. Basically, you optimize around the edges and do not attack any of the sacred cows (typically meaning you do not touch either engineering or sales). The gains are minimal, and the bottlenecks that are holding you back are still deeply in place. Ginny Rometti made a version of this point in one of IBM’s earnings calls, but so could every other Tech 50 CEO in any given quarter. This is a really big problem because tech has never been good at optimization.

- The innovation project blended two or more goals. The problem here is that either the differentiation goal slowed you down or the neutralization goal dumbed you down or the optimization goal tied you down. One way or another, you went down.

So the net here is simple. Managing innovation is a different discipline from innovating per se. It is all about controlling the charter, targeting one and only one kind of return, and then focusing the team solely on that set of outcomes. It isn’t all that cool. It is just very, very important.

That’s what I think. What do you think?

Image Credit: Pexels

![]() Sign up here to join 17,000+ leaders getting Human-Centered Change & Innovation Weekly delivered to their inbox every week.

Sign up here to join 17,000+ leaders getting Human-Centered Change & Innovation Weekly delivered to their inbox every week.

Pingback: Top 10 Human-Centered Change & Innovation Articles of August 2023 | Human-Centered Change and Innovation