The Customer Experience Failures Silently Draining Your P&L

by Braden Kelley and Art Inteligencia

Revenue leakage is one of the most widely discussed topics in finance and operations — and one of the most narrowly defined. Ask most CFOs what revenue leakage means and they will describe billing errors, missed invoices, and contract compliance gaps. These are real problems worth solving. But they represent only the visible surface of a much larger issue.

The revenue leakage that does the most damage to most organizations is not found in the billing system. It is found in the customer experience — in the friction, failed moments, and unmet expectations that cause customers to buy less, expand less, renew less, and advocate less than they would if their experience were better. This form of revenue leakage is invisible in most financial reports. It shows up in churn rates, in Net Promoter Scores, in declining share of wallet, and in the slow erosion of customer lifetime value that compounds quietly over years.

This article addresses both: the operational revenue leakage that finance teams understand, and the experience revenue leakage that most organizations are leaving on the table without realizing it.

What is Revenue Leakage?

Revenue leakage is the gap between the revenue an organization should be capturing and the revenue it actually captures. The standard formula is:

Revenue Leakage % = (Total Potential Revenue − Actual Collected Revenue) ÷ Total Potential Revenue × 100

Industry benchmarks suggest that leakage under 3% is excellent, 3–5% is acceptable, and above 5% requires immediate attention. For a $100M revenue business, 5% leakage represents $5M walking out the door annually — before any consideration of the experience-driven leakage that rarely appears in these calculations at all.

Two Types of Revenue Leakage — and Why Most Organizations Only See One

Type 1: Operational Revenue Leakage

Operational revenue leakage is the form most commonly discussed in finance and RevOps contexts. It includes:

- Billing errors — incorrect charges, missed charges, duplicate invoices, and pricing discrepancies between what was contracted and what was billed

- Unbilled services — work performed or value delivered that was never invoiced, often due to disconnected systems between service delivery and billing

- Contract compliance gaps — discounts that were meant to be temporary becoming permanent, usage overages that were never billed, and renewal terms that weren’t enforced

- Failed collections — invoices issued but not collected due to expired payment methods, billing contact churn, or inadequate dunning processes

- Handoff failures — context and commitments lost between sales, implementation, and customer success teams that result in under-delivering against what was sold

This form of leakage is well understood and increasingly addressable through better billing infrastructure, contract management systems, and revenue operations discipline. It is important and worth fixing. It is also, in most organizations, the smaller of the two leakage problems.

Type 2: Experience Revenue Leakage

Experience revenue leakage is the revenue an organization fails to capture — or actively destroys — because of failures in the customer experience. It is the harder-to-see, harder-to-measure, and almost always larger form of revenue leakage. It includes:

- Churn driven by experience failure — customers who cancel, don’t renew, or stop purchasing because their experience fell below expectations, not because they found a cheaper alternative

- Expansion revenue never realized — customers who could have bought more, upgraded, or expanded their relationship but didn’t because their experience gave them no reason to

- Referrals never given — customers who would have recommended you to peers but didn’t because their experience was merely adequate rather than genuinely excellent

- Repurchase cycles shortened or broken — customers who bought less frequently or in smaller amounts because friction in the experience made doing more business with you feel like more effort than it was worth

- Price sensitivity artificially elevated — customers who demanded discounts or pushed back on pricing not because your prices were genuinely too high, but because the experience didn’t justify the value you were charging for

- Recovery costs from poor experiences — the service calls, refunds, make-goods, and relationship repair investments required to address experience failures that should never have occurred

None of these show up cleanly in a billing audit. They are diffuse, difficult to attribute, and invisible in most financial reporting. But their combined scale is enormous. Bain & Company research found that companies that excel at customer experience grow revenues 4–8% above their market — meaning the gap between average and excellent experience represents revenue leakage of that magnitude for every organization that isn’t at the top.

The Six Experience Failures That Drive the Most Revenue Leakage

1. The onboarding gap

The period immediately after purchase is the highest-risk window for experience revenue leakage. Customers arrive with expectations shaped by the sales process and are immediately confronted with the reality of onboarding — which is almost always harder, slower, and more confusing than what they were led to expect. Customers who never fully succeed with onboarding rarely expand, rarely renew enthusiastically, and frequently churn at the first renewal. The revenue lost to poor onboarding is rarely attributed to onboarding — it shows up months later as churn or non-renewal.

2. The service experience valley

Every customer relationship encounters service moments — billing questions, support issues, complaints, and problems that need resolving. These moments are disproportionately important to the overall experience because they are emotionally charged. A service experience handled badly damages trust in a way that no amount of good routine experience can quickly repair. The “service recovery paradox” — where a problem handled exceptionally well can produce higher loyalty than if no problem had occurred — is real, but it requires genuinely excellent recovery, not just adequate resolution. Most organizations deliver adequate. The gap between adequate and excellent is where experience revenue leakage lives.

3. The value realization gap

Customers who don’t fully realize the value they purchased don’t expand their relationship and are easy to lose. Value realization gaps are pervasive — they exist in virtually every B2B and B2C relationship where the product or service requires any customer effort to deliver its benefits. Organizations that actively help customers realize value retain more, expand more, and generate more referrals. Organizations that deliver the product and move on leave the value realization gap unfilled and lose the revenue that would have followed from success.

4. The friction tax

Friction accumulates across the customer journey in ways that are individually minor but collectively significant. Difficult processes, confusing interfaces, slow response times, unnecessary steps, and inconsistent experiences across channels all add to the friction tax customers pay to do business with you. As friction accumulates, customers do less: they buy less often, buy less per transaction, engage less with expansion opportunities, and recommend less enthusiastically. The revenue impact of accumulated friction is diffuse and hard to measure — which is exactly why it persists.

5. The consistency failure

Customers who have excellent experiences in some channels and poor experiences in others trust you less than customers who have consistently good experiences everywhere. Inconsistency is particularly damaging because it creates uncertainty — customers don’t know which version of your organization they are going to encounter. Uncertainty suppresses engagement. Customers who are uncertain about their experience buy less, recommend less, and churn more readily when alternatives present themselves.

6. The relationship void

Organizations that treat customers as transactions rather than relationships systematically leave expansion revenue on the table. Customers who feel known, understood, and valued by their providers spend more, stay longer, and are far more resistant to competitive alternatives. Most organizations are not building relationships — they are processing transactions and calling the result a customer relationship. The revenue gap between transactional and relational customer management is measurable and substantial.

How to Identify Experience Revenue Leakage in Your Organization

Operational revenue leakage can be found through billing audits and contract reviews. Experience revenue leakage requires a different diagnostic approach — one that starts with the customer experience rather than the financial systems.

The most direct method is a customer experience audit — a systematic, human-centered evaluation of how customers actually experience your organization across every channel and touchpoint. An experience audit identifies the specific friction points, service experience failures, value realization gaps, and consistency failures that are driving the revenue leakage your P&L can’t fully explain.

Unlike financial audits that work backwards from revenue data, an experience audit works forward from the customer journey — finding the failures before they fully show up in the numbers. This is critical because experience revenue leakage compounds: a poor onboarding experience in month one doesn’t show up in revenue until month twelve when the renewal doesn’t happen. By the time the financial signal is visible, the customer relationship damage has been accumulating for a year.

Specific diagnostic questions an experience audit answers:

- Where in the customer journey are the highest-friction moments — the ones customers endure without complaint but that silently reduce their willingness to expand or renew?

- Which service experience failures are occurring most frequently, and how well are they being recovered from?

- Are customers actually achieving the outcomes they purchased for, or is there a systematic value realization gap in specific segments or use cases?

- How consistent is the experience across channels — and where are the inconsistency gaps largest?

- How does the experience compare to key competitors — and where are you losing on experience quality rather than price?

Quantifying Experience Revenue Leakage

One of the reasons experience revenue leakage persists is that it is difficult to attach a specific number to it. Unlike billing errors, which have a clear dollar value, experience revenue leakage shows up indirectly — in churn rates, expansion rates, NPS scores, and competitive win/loss ratios. But it can be quantified with the right framework.

The Customer Experience Revenue Leakage diagnostic — part of the Experience Audit methodology — maps specific experience failures to their estimated revenue impact across five dimensions: churn contribution, expansion revenue foregone, referral revenue foregone, service recovery cost, and price sensitivity premium. This produces a prioritized estimate of where experience investment will generate the highest financial return — giving CFOs and CX leaders a common language for making the case for experience improvement investment.

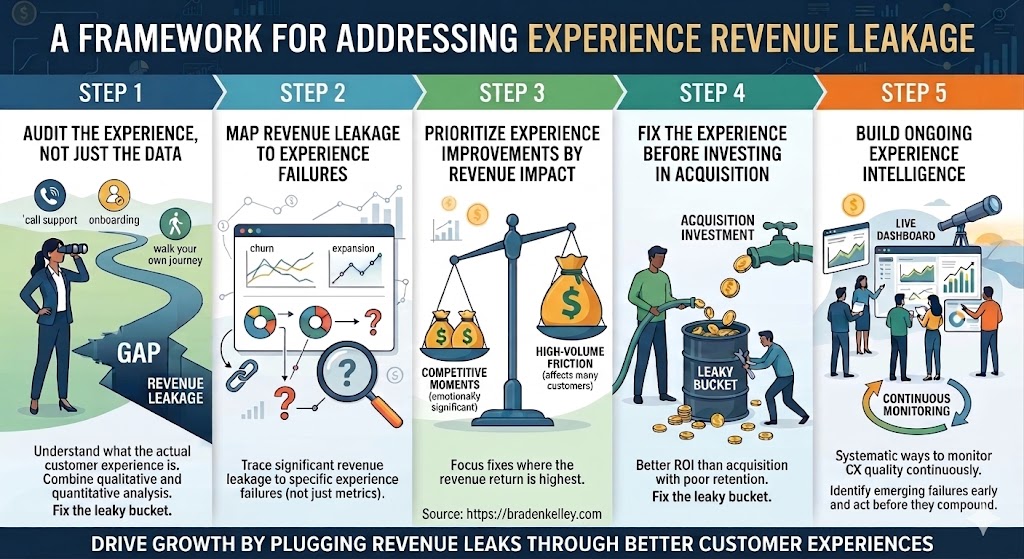

A Framework for Addressing Experience Revenue Leakage

Step 1: Audit the experience, not just the data

Before investing in retention programs, expansion campaigns, or NPS improvement initiatives, understand what the actual customer experience is. Walk your own journey. Call your own support line. Go through your own onboarding as a new customer. The gap between what you think the experience is and what it actually is almost always contains the most important revenue leakage.

Step 2: Map revenue leakage to experience failures, not to revenue metrics

For each significant revenue leakage source — high churn in a specific segment, low expansion in a specific cohort, low NPS in a specific channel — trace it back to the specific experience failures most likely driving it. This requires qualitative research, not just quantitative analysis.

Step 3: Prioritize experience improvements by revenue impact

Not all experience failures drive equal revenue leakage. Prioritize fixes that address high-volume friction (affecting many customers), high-stakes moments (emotionally significant interactions), and competitive gaps (experiences where alternatives are measurably better).

Step 4: Fix the experience before investing in acquisition

The most common and expensive mistake in revenue management is investing heavily in customer acquisition while experience failures are driving significant leakage. Fixing the leaky bucket before pouring more water in consistently delivers better ROI than acquisition investment against a poor retention foundation.

Step 5: Build ongoing experience intelligence

Experience revenue leakage is not a one-time problem to be solved — it is an ongoing management challenge. Organizations that achieve consistently low leakage have built systematic ways to monitor customer experience quality continuously, identify emerging failures early, and act on them before they compound into significant revenue impact.

Frequently Asked Questions About Revenue Leakage

What is revenue leakage?

Revenue leakage is the gap between the revenue an organization should be capturing and the revenue it actually captures. It includes both operational leakage — billing errors, unbilled services, contract compliance gaps, and failed collections — and experience leakage — the revenue lost because customer experience failures drive churn, suppress expansion, prevent referrals, and erode price realization. Most definitions of revenue leakage focus exclusively on operational causes, significantly underestimating the total revenue impact. The formula is: Revenue Leakage % = (Total Potential Revenue − Actual Collected Revenue) ÷ Total Potential Revenue × 100.

What causes revenue leakage?

Revenue leakage has two primary categories of causes. Operational causes include billing errors, missed charges, contract compliance failures, failed payment collections, and handoff failures between sales and service teams. Experience causes — which are typically larger in total impact but less visible — include poor onboarding that prevents value realization, service experience failures that damage trust and accelerate churn, friction accumulation across the customer journey that suppresses expansion and repurchase, inconsistent cross-channel experiences that undermine confidence, and transactional rather than relational customer management that leaves expansion revenue uncaptured.

How do you identify revenue leakage?

Operational revenue leakage is identified through billing audits, contract reviews, and revenue operations analysis. Experience revenue leakage requires a different diagnostic approach — specifically, a customer experience audit that walks the actual customer journey to identify the friction points, service failures, value realization gaps, and consistency failures driving churn, suppressing expansion, and eroding customer lifetime value. Financial data can signal that experience revenue leakage exists; only customer experience research can identify where it lives and what is causing it.

What is the difference between revenue leakage and customer churn?

Customer churn is one specific form of revenue leakage — the revenue lost when customers stop doing business with you entirely. Revenue leakage is a broader concept that includes churn but also encompasses revenue lost from customers who stay but buy less, expand less, refer less, and pay less than they would if their experience were better. A customer who renews but never expands their relationship, who would have recommended you but doesn’t, or who accepts your full price reluctantly rather than willingly — all of these represent revenue leakage that doesn’t show up in churn metrics but is nonetheless real and quantifiable.

How does a customer experience audit identify revenue leakage?

A customer experience audit identifies experience revenue leakage by walking the actual customer journey across all channels and touchpoints — finding the specific friction points, service failures, value realization gaps, and consistency failures that are driving revenue loss your financial reports can’t fully explain. Unlike data analysis that works backwards from revenue metrics, an experience audit works forwards from the customer journey (going beyond customer journey mapping), finding failures before they fully compound into financial impact. The result is a prioritized map of experience improvements ranked by their estimated revenue impact — giving leaders a clear, actionable roadmap for fixing the experience failures that are silently draining the P&L.

Ready to find the experience failures driving revenue leakage in your organization? Learn more about the Experience Audit →

Image credits: Google Gemini

Content Authenticity Statement: The topic area, key elements to focus on, etc. were decisions made by Braden Kelley, with a little help from Google Gemini to clean up the article, add images and create infographics.

![]() Sign up here to get Human-Centered Change & Innovation Weekly delivered to your inbox every week.

Sign up here to get Human-Centered Change & Innovation Weekly delivered to your inbox every week.